Fama French Finance

Fama-French: Expanding Capital Asset Pricing

The Fama-French models are influential asset pricing models that build upon the Capital Asset Pricing Model (CAPM). Developed by Eugene Fama and Kenneth French, these models attempt to provide a more accurate description of expected stock returns than the CAPM, which solely considers a single factor: market risk.

The CAPM Shortcomings

The CAPM, while theoretically elegant, often struggles to explain real-world stock returns. It posits that a stock's expected return is linearly related to its beta, a measure of its systematic risk relative to the market. However, empirical evidence has shown that other factors besides beta can significantly influence returns, leading to what are known as "anomalies." Fama and French sought to address these shortcomings.

The Three-Factor Model

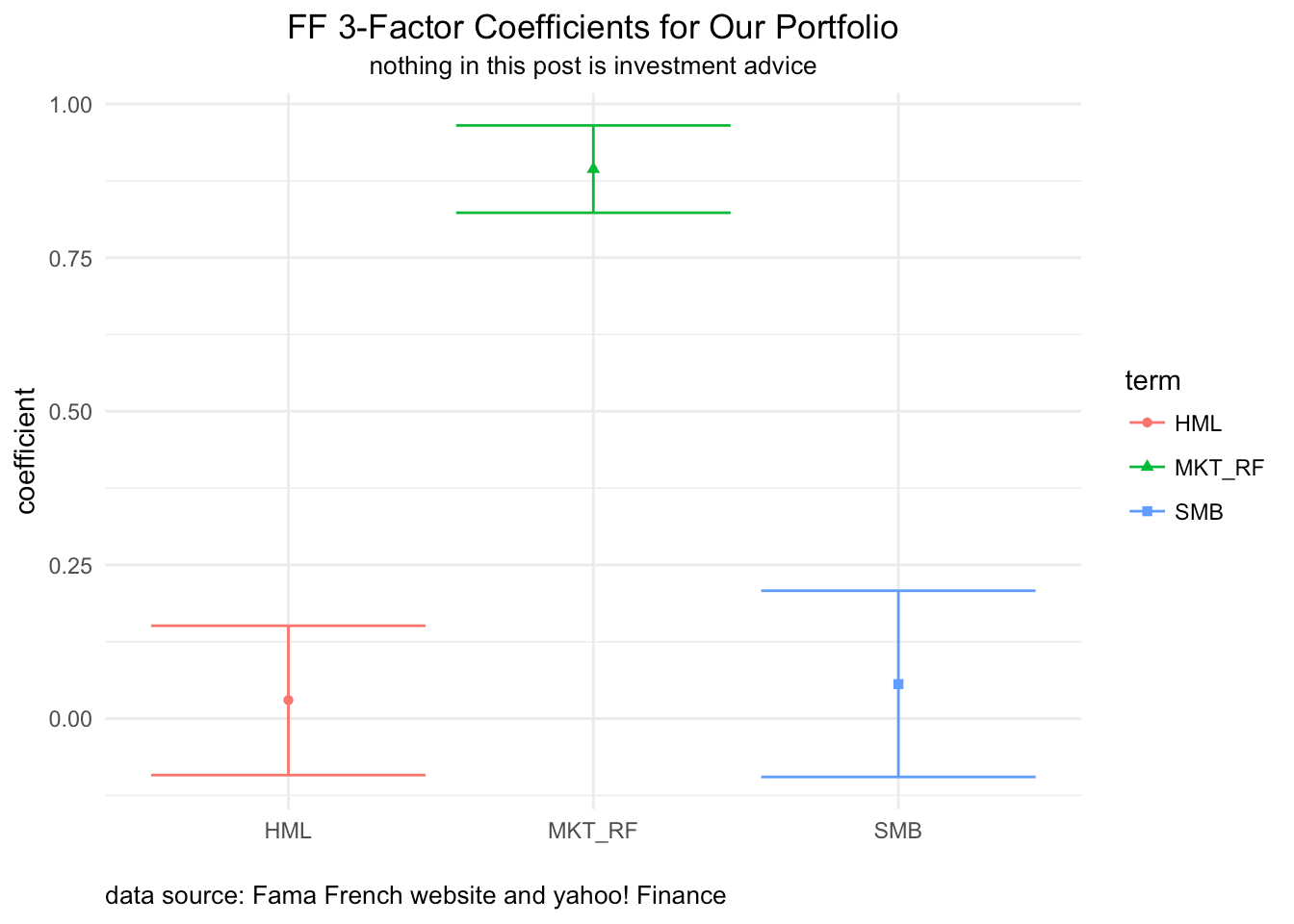

The Fama-French three-factor model, introduced in their 1993 paper, adds two factors to the CAPM: size (SMB - Small Minus Big) and value (HML - High Minus Low). Size refers to the tendency of small-cap stocks to outperform large-cap stocks over long periods. Value refers to the tendency of value stocks (those with high book-to-market ratios) to outperform growth stocks (those with low book-to-market ratios). The three-factor model equation is:

E(Ri) = Rf + βi(Rm - Rf) + si(SMB) + hi(HML)

Where:

- E(Ri) is the expected return of asset i

- Rf is the risk-free rate

- βi is the beta of asset i (market risk)

- Rm is the market return

- SMB is the size premium (return of small-cap stocks minus return of large-cap stocks)

- HML is the value premium (return of high book-to-market stocks minus return of low book-to-market stocks)

- si is the coefficient for SMB, representing the sensitivity of asset i to size

- hi is the coefficient for HML, representing the sensitivity of asset i to value

This model suggests that stocks with higher betas, smaller market capitalizations, and higher book-to-market ratios tend to have higher expected returns. It's widely used by investors to evaluate portfolio performance and identify potentially undervalued stocks.

The Five-Factor Model

In 2015, Fama and French introduced a five-factor model, adding profitability (RMW - Robust Minus Weak) and investment (CMA - Conservative Minus Aggressive) factors to the existing three. Profitability refers to the tendency of more profitable firms to outperform less profitable ones. Investment refers to the tendency of firms that invest conservatively to outperform firms that invest aggressively.

This extension aimed to further explain anomalies not captured by the three-factor model. While generally performing well, some research suggests that the five-factor model may not always outperform the three-factor model, especially in certain markets.

Criticisms and Limitations

Despite their widespread use, Fama-French models face criticisms. Some argue that the size and value premiums are simply empirical observations without a strong theoretical foundation, potentially representing data mining or behavioral biases rather than rational risk factors. Furthermore, the models are backward-looking and may not accurately predict future returns, as factor premiums can vary over time. The addition of factors has also faced criticism of overfitting the data.

Conclusion

The Fama-French models represent a significant advancement in asset pricing theory. By incorporating size, value, profitability, and investment factors, they offer a more nuanced explanation of expected stock returns than the CAPM. While not without limitations, they remain a valuable tool for investors and academics seeking to understand the complexities of financial markets.

961×1024 fama french factor model diagram from www.pinterest.com

961×1024 fama french factor model diagram from www.pinterest.com  277×135 fama french masters finance hq from msfhq.com

277×135 fama french masters finance hq from msfhq.com  1024×1024 tidy finance comparing fama french factors from www.tidy-finance.org

1024×1024 tidy finance comparing fama french factors from www.tidy-finance.org  705×359 fama french factor model breaking finance from breakingdownfinance.com

705×359 fama french factor model breaking finance from breakingdownfinance.com  1024×682 fama french model learnsignal from www.learnsignal.com

1024×682 fama french model learnsignal from www.learnsignal.com  670×425 fama french factors hhsse stockholm school economics from www.hhs.se

670×425 fama french factors hhsse stockholm school economics from www.hhs.se  1432×798 sizevalue from www.calculatinginvestor.com

1432×798 sizevalue from www.calculatinginvestor.com  262×394 fama french qa carbon financial from carbonfinancial.co.uk

262×394 fama french qa carbon financial from carbonfinancial.co.uk  880×498 ten simple lessons fama french valideas guru investor blog from blog.validea.com

880×498 ten simple lessons fama french valideas guru investor blog from blog.validea.com  1060×486 closer fama french idx insights from idxinsights.com

1060×486 closer fama french idx insights from idxinsights.com  1366×649 quantitative trading fama french factors indian stock markets from quantcity.blogspot.com

1366×649 quantitative trading fama french factors indian stock markets from quantcity.blogspot.com  1024×576 celebrating groundbreaking research giants finance fama from www.ifa.com

1024×576 celebrating groundbreaking research giants finance fama from www.ifa.com  850×551 investment opportunities fama french scientific from www.researchgate.net

850×551 investment opportunities fama french scientific from www.researchgate.net  1024×692 fama french factor models from www.rebellionresearch.com

1024×692 fama french factor models from www.rebellionresearch.com  967×327 estimating stock returns fama french factor model python from medium.com

967×327 estimating stock returns fama french factor model python from medium.com  1219×508 fama french model from alphaarchitect.com

1219×508 fama french model from alphaarchitect.com  1344×960 introduction fama french views from rviews.rstudio.com

1344×960 introduction fama french views from rviews.rstudio.com  700×530 performance fama french factor returns isabelnet from www.isabelnet.com

700×530 performance fama french factor returns isabelnet from www.isabelnet.com  995×565 fama french factor asset pricing model breaking treadmill from breakingthetreadmill.com

995×565 fama french factor asset pricing model breaking treadmill from breakingthetreadmill.com  720×540 fama french factor model theoretical conceptual from www.slideserve.com

720×540 fama french factor model theoretical conceptual from www.slideserve.com  1132×509 fama french multi factor models sell side handbook from sellsidehandbook.com

1132×509 fama french multi factor models sell side handbook from sellsidehandbook.com  750×472 fama french auld lang syne from www.brightscope.com

750×472 fama french auld lang syne from www.brightscope.com  768×434 fama french model key factors applications business school from esoftskills.com

768×434 fama french model key factors applications business school from esoftskills.com  850×638 figure returns fama french industry portfolios green from www.researchgate.net

850×638 figure returns fama french industry portfolios green from www.researchgate.net